Last updated

Low credit scores, charge-offs, and collections do not have to mean another denial. We identify Dallas-Fort Worth apartment communities with flexible credit requirements, confirm their criteria directly with the property manager, and send you a custom list of homes that will actually consider your application. No more wasting non-refundable application fees on a property that was never going to say yes.

Renting in DFW With Bad Credit, Honestly Explained

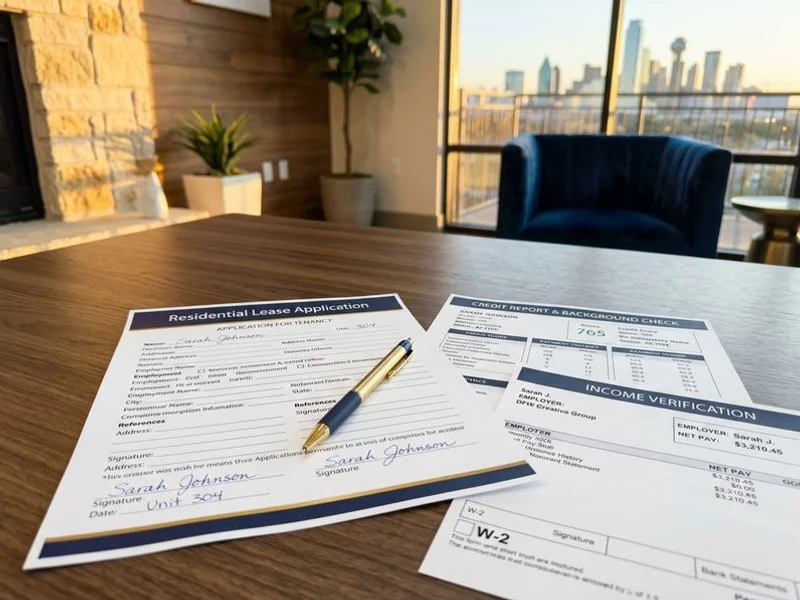

Finding a DFW apartment with bad credit means wading through communities that will reject you and wasting non-refundable application fees along the way. Our bad credit apartment locating service cuts through that by targeting communities that actually work with challenged credit, then verifying their criteria before you apply.

Most DFW property managers run your background through one of three bureaus, which are Equifax, Experian, or TransUnion. They weigh your FICO Score or VantageScore against their specific community rules. We know exactly which properties offer leniency.

A score that triggers a hard denial at one complex can actually clear conditional approval right next door. The credit score is rarely the entire story in the Texas rental market.

Our experts understand that communities using hybrid screening criteria also evaluate your debt-to-income (DTI) ratio and your gross monthly income.

- These properties check whether any charge-offs or active collections are old, paid down, or current.

- A few amazing spots will skip the credit check entirely in exchange for a higher deposit or a risk fee.

We are going to walk you through the exact steps used to get you approved quickly and easily.

What We Look at Before Pulling Your List

The recent surge in new apartment supply across the DFW area has actually worked in your favor. Thousands of new units hit the market between 2025 and 2026, pushing many property managers to relax their strict criteria to fill empty rooms. Our team reviews your specific details thoroughly to take advantage of these new opportunities.

This careful initial review prevents wasted application fees and frustrating auto-decline scenarios. A complete picture of your situation allows a direct path to the communities that will actually say yes. We analyze the following factors to build your custom property list:

- Score range and report state: Property managers check what shows on Equifax, Experian, and TransUnion. If your score falls between 600 and 649, many places will approve you with just a moderate $200 to $400 deposit.

- Charge-offs and collections: We look at the details here, such as current versus paid status, the original creditor, and the exact amount owed.

- Rental history: Any past issues that affect your tenant screening report need to be addressed upfront, though older evictions are often overlooked. Alternative documents or W-2s must show your gross monthly income is at least three times the base rent.

- Move-in budget: Our locators verify all of these details to present you in the best possible light.

Your move-in budget dictates the realistic options available to you. Accurate quotes for risk fees and conditional-approval deposits ensure you never face surprise costs on moving day.

When Conditional Approval Is the Right Path

We see many DFW communities happily approve an applicant under conditional terms if their credit score is low. These conditions act as a safety net for the property manager while giving you a chance to secure a great home. The most common conditional requirements fall into three distinct categories.

Our agents always verify the specific conditional terms required by each property before you submit an application. This transparent approach ensures the final move-in number fits your bank account.

Common Conditional Approval Costs

Property managers use three primary conditional requirements to offset potential losses. We break down these options clearly so you can prepare your finances.

A risk fee is a very popular option, usually ranging from $250 to $500 as a one-time non-refundable charge. A double security deposit is another frequent requirement for renters rebuilding their profiles. Our team notes that this option is fully refundable at the end of your lease, but it requires a lot more cash upfront.

The average rent in Dallas hit $2,233 recently, meaning a double deposit could easily pull over $4,400 from your savings. Luxury second-chance approvals often ask for a higher first-month or last-month rent requirement instead of standard deposits. We provide these numbers clearly in a simple comparison table.

| Approval Type | Typical Upfront Requirement | Refundable Status | Average Cost in Dallas |

|---|---|---|---|

| Standard Approval | Standard Deposit | Yes | $200 - $400 |

| Risk Fee Pathway | One-Time Fee | No | $250 - $500 |

| Deposit Pathway | Double Security Deposit | Yes | $2,000 - $4,500+ |

Frequently Searched Communities and Situations

Every single neighborhood across the Metroplex features a totally different approval climate. The suburbs north of Dallas, like Frisco and Plano, generally enforce the strictest screening guidelines. Our agents find that cities like Arlington and Grand Prairie serve as the friendliest landing zones for renters.

Those mid-city areas balance great amenities with much more forgiving property managers. South Dallas and the Pleasant Grove area also offer a massive amount of inventory for second-chance leasing right now. We have successfully placed clients in beautiful communities across the entire urban core, including Uptown, Oak Lawn, the Medical District, Deep Ellum, and Oak Cliff.

Finding the Right Neighborhood Fit

Tarrant County actually boasts over 59 broken-lease friendly apartment communities. This makes the western side of the Metroplex highly attractive if you have past rental debt. Our database constantly tracks which specific neighborhoods accept specific background issues.

A strategic location choice can completely change your odds of approval. Applying to strict buildings in Uptown without guidance will just drain your bank account through non-refundable application fees.

Our service points you directly toward the welcoming properties to save you time.

If you are early in the process, the 2026 Second Chance Apartment Search Guide walks through the whole approach. This helpful resource covers everything you need to know about the current market.

Pair Bad Credit Locating With a Guarantor When It Helps

We highly recommend exploring a third-party service if your income alone cannot clear the property’s requirements. A lease guarantor company acts like a corporate co-signer on demand for your rental application. Instead of asking a family member to back your lease, you pay a specialized business to guarantee the rent. Our team frequently works with industry leaders like TheGuarantors, Rhino, and LeaseLock to get tough applications approved.

How Guarantor Pricing Works

The costs for these third-party approvals vary wildly based on the provider and your specific profile. A policy from TheGuarantors typically ranges from 40 percent to 130 percent of one month’s rent as an upfront fee. Our clients on a strict budget often prefer Rhino, which offers monthly security deposit insurance policies for as little as four dollars a month.

These alternative deposit programs keep your hard-earned cash in your pocket during an expensive move. LeaseLock integrates directly into the property’s software to eliminate traditional deposits entirely. We will gladly compare the math for your specific situation to find the cheapest route.

- You can review a detailed breakdown in Bad Credit vs Guarantor: Which Approval Path Fits You? to see the side-by-side numbers.

- You can also jump straight to Guarantor & Co-Signer Apartment Locating when you are ready to start touring.

Our apartment locating experts are standing by to make your move completely effortless and rewarding.